Australia’s sustainability reporting landscape has been transformed. What was once a voluntary exercise in stakeholder communication is now a mandatory compliance obligation for a growing range of entities — and the framework, timeline and consequences of non-compliance are more complex than many boards and management teams appreciate.

This guide provides a complete, current overview of sustainability reporting requirements and best practice for Australian businesses in 2026 — covering mandatory obligations under AASB S1 and AASB S2, the voluntary GRI framework, and the specific disclosure requirements for climate, modern slavery, gender equality and greenhouse gas emissions.

For the broader ESG context, read our complete guide to ESG in Australia.

Why Sustainability Reporting Matters

Sustainability reporting serves multiple purposes simultaneously. For regulators, it provides accountability for environmental and social commitments. For investors, it provides decision-relevant information on ESG risks and opportunities. For customers and communities, it provides transparency on corporate impacts. And for management, a disciplined reporting process surfaces data, identifies gaps and drives improvement in a way that informal sustainability management does not.

The shift to mandatory reporting in Australia — particularly through AASB S2 — has elevated sustainability disclosure from a communications exercise to a regulated activity with legal accountability equivalent to financial reporting. This changes the bar for data quality, governance processes and external assurance.

AASB S1: General Sustainability Disclosures

AASB S1 — General Requirements for Disclosure of Sustainability-related Financial Information — is Australia’s adoption of the ISSB’s IFRS S1 standard. It establishes the overarching framework and requirements for sustainability-related financial information disclosures.

AASB S1 requires entities to disclose information about all sustainability-related risks and opportunities that could reasonably be expected to affect the entity’s prospects. Key requirements include:

- Disclosures about governance of sustainability-related risks and opportunities

- Information about how sustainability-related risks and opportunities affect the entity’s strategy and business model

- How sustainability-related risks are identified, assessed and managed

- Metrics and targets used to monitor sustainability-related performance and progress

AASB S1 applies initially to climate-related disclosures (via AASB S2), with the expectation that broader sustainability-related disclosures will follow as the framework matures.

AASB S2: Climate-related Disclosures

AASB S2 — Climate-related Disclosures — is the centrepiece of Australia’s mandatory sustainability reporting framework. It is based on the ISSB’s IFRS S2 and is closely aligned with the TCFD framework. For Group 1 entities, AASB S2 applies to annual reporting periods beginning on or after 1 January 2025.

Who Is Covered by AASB S2?

The three-group staging for AASB S2 mandatory reporting is:

- Group 1: Entities required to lodge financial reports under Chapter 2M of the Corporations Act that are large listed entities, large financial institutions, registered schemes, and RSE licensees meeting size thresholds. Reporting from 1 January 2025.

- Group 2: Other large Corporations Act reporters — unlisted public companies, large proprietary companies and foreign companies meeting size thresholds (consolidated revenue ≥$500M, consolidated gross assets ≥$1B, or average employees ≥500). Reporting from 1 July 2026.

- Group 3: Other Corporations Act reporters meeting lower size thresholds (consolidated revenue ≥$50M, consolidated gross assets ≥$25M, or average employees ≥100). Reporting from 1 July 2027.

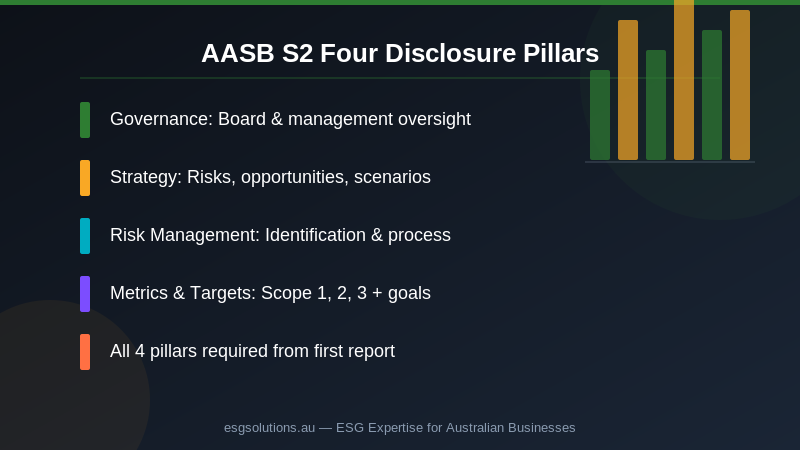

What AASB S2 Requires

AASB S2 disclosures are structured around four pillars:

Governance: Describe the board’s oversight of climate-related risks and opportunities — which body or individual at board level holds oversight responsibility, how climate competency is maintained, and how management’s climate-related processes are supervised. Describe management’s role in assessing and managing climate-related risks and opportunities.

Strategy: Describe the climate-related risks and opportunities identified that could reasonably be expected to affect your business over the short, medium and long term. Describe the actual and anticipated effects on your business model, strategy and financial planning. Include the results of climate scenario analysis — testing strategy resilience under at least a 1.5°C warming scenario and a higher-warming scenario.

Risk Management: Describe your processes for identifying, assessing and prioritising climate-related risks, and how these processes are integrated with your overall enterprise risk management.

Metrics and Targets: Disclose cross-industry metrics including Scope 1, 2 and (after transition relief) Scope 3 GHG emissions; the percentage of assets or business activities vulnerable to climate-related transition and physical risks; and the amount of capital deployed toward climate-related opportunities. Disclose the climate-related targets you have set and your progress against them.

Transition Relief Provisions

AASB S2 includes several transition relief provisions to give entities time to build their data and governance capabilities:

- Scope 3 emissions disclosure is deferred for one year after an entity first becomes required to report

- Scenario analysis disclosures receive some transitional flexibility in the first year

- Comparative information requirements are phased in

- Assurance requirements begin at limited assurance and phase up to reasonable assurance over time

These reliefs are transitional, not permanent. Building your data collection, verification and governance processes during the relief period ensures you’re not scrambling when the full requirements bite.

GRI Standards: The Voluntary Benchmark

The Global Reporting Initiative (GRI) Standards are the world’s most widely used sustainability reporting framework — and Australia’s most commonly adopted voluntary ESG reporting framework. GRI provides standards covering universal topics (governance, strategy, stakeholder engagement, materiality) and specific topics across environmental (energy, emissions, water, biodiversity, waste) and social (employment, OHS, human rights, community, anti-corruption) dimensions.

GRI Reporting Options

GRI offers two reporting options. GRI With Reference means the report references GRI standards but does not follow all requirements systematically. In Accordance with GRI requires full compliance with the GRI Universal Standards (2021) and disclosure of all applicable topic-specific standards determined through a materiality assessment. The In Accordance option provides the strongest credibility signal.

GRI and AASB S2: How They Relate

GRI and AASB S2 are complementary, not competing. GRI provides broader ESG coverage across environmental, social and governance topics — including many issues not covered by AASB S2’s current climate focus. AASB S2 provides more rigorous, financially-oriented climate disclosure with mandatory status and legal accountability. Most large Australian organisations use both: GRI for their annual sustainability report and AASB S2 for climate disclosures integrated into their financial reporting.

Other Australian Mandatory Reporting Frameworks

Modern Slavery Statements

Annual Modern Slavery Statements are required under the Modern Slavery Act 2018 for Australian entities with annual consolidated revenue of $100M or more. Statements must be published on the Australian Border Force’s Modern Slavery Register and address six mandatory criteria. Quality statements go beyond compliance boilerplate to include specific risk assessment findings, concrete actions taken, and credible effectiveness evaluation.

WGEA Reporting

Private sector employers with 100 or more employees must submit an annual report to WGEA covering the six gender equality indicators. Since 2024, WGEA publishes employer-level gender pay gap data publicly — making this one of the most reputationally significant social disclosures for affected employers. A proactive approach to pay equity analysis and gap remediation before WGEA reporting dates is strongly advisable.

NGER Reporting

The National Greenhouse and Energy Reporting (NGER) Act requires corporations meeting greenhouse gas emissions and/or energy production and consumption thresholds to report annually to the Clean Energy Regulator. NGER data forms the basis for Safeguard Mechanism compliance and provides the emissions inventory that underpins AASB S2 Scope 1 and 2 disclosures for covered entities.

Building a Sustainability Reporting Program

Developing a credible, compliant and commercially useful sustainability reporting program requires systematic attention to four elements.

Data Infrastructure

Sustainability reporting is only as good as the underlying data. Building the data collection systems, verification processes and controls necessary for AASB S2 climate data requires investment in technology, process design and governance. Many organisations underestimate this element until they’re under reporting deadline pressure. The sooner you start building your data infrastructure, the better your first mandatory report will be.

Governance and Accountability

AASB S2 disclosures have the same legal accountability as financial statements — meaning they are subject to the Corporations Act’s prohibition on misleading or deceptive statements. Board members and executives who approve AASB S2 disclosures need confidence that the underlying data and methodology are robust. This requires clear accountability for ESG data at management level, board oversight processes and — ultimately — external assurance.

External Assurance

AASB S2 requires limited assurance of climate disclosures initially, phasing up to reasonable assurance over time. External assurance — provided by an accredited auditor — tests the accuracy and completeness of your sustainability data and the robustness of your disclosure processes. Preparing for assurance early means building the data trails, internal controls and documentation that assurance processes require.

Materiality Process

A documented, credible materiality process is the foundation of defensible sustainability reporting. It demonstrates that you have systematically identified the topics most significant to your business and stakeholders — and that your disclosures are prioritised accordingly. AASB S2 applies a financial materiality lens; GRI applies a double materiality lens. Both require stakeholder engagement as an input.

Common Sustainability Reporting Mistakes

The most frequent sustainability reporting failures in Australia fall into three categories.

Unsubstantiated claims: ASIC has made greenwashing enforcement a priority, and INFO 271 is clear that sustainability claims — whether in annual reports, marketing materials or investor presentations — must be specific, accurate and supported by evidence. Vague commitments (“we are committed to sustainability”) without supporting data and specific targets are both legally risky and commercially unconvincing.

Poor data quality: Emissions inventories built on estimates and assumptions without clear methodology, GHG data that changes materially between years without explanation, and social metrics that aren’t consistent across reporting periods — these data quality issues create assurance challenges and undermine report credibility.

Reporting disconnected from strategy: A sustainability report that documents activities but doesn’t connect to a coherent strategy, meaningful targets and genuine management commitment reads as a compliance exercise rather than a strategic communication. Sophisticated investors and institutional customers can tell the difference.

Download Our Free ESG Reporting Checklist

Preparing for AASB S2 compliance and building a credible sustainability reporting program requires systematic attention to governance, data, methodology and communication. Our ESG Reporting Checklist provides a structured, actionable framework for Australian businesses at every stage of reporting maturity.

ESG Solutions works with Australian businesses to design, implement and assurance-ready their sustainability reporting programs — from first-time GRI reporters through to listed entities preparing for mandatory AASB S2 disclosures.

Download our Free ESG Reporting Checklist today and start building your reporting program on solid foundations.