ESG has shifted from a voluntary aspiration to a legal and commercial imperative for Australian businesses — faster than most boards anticipated.

Mandatory climate disclosures are now embedded in Australian law. ASIC is actively pursuing greenwashing. APRA has integrated climate risk into prudential supervision. And investors, customers and employees are scrutinising corporate ESG commitments with increasing sophistication. The question is no longer whether Australian businesses need an ESG strategy — it’s whether yours is credible enough to withstand scrutiny.

This guide covers everything you need to understand, build and communicate your ESG position in Australia. Whether you’re a listed company preparing for mandatory AASB S2 disclosures or an SME taking its first practical steps, you’ll find a clear, Australian-context framework here.

What Is ESG? Understanding the Three Pillars

ESG stands for Environmental, Social and Governance — three interconnected pillars that together define how a business manages its impacts, risks and responsibilities beyond financial performance alone.

Environmental

The environmental pillar covers your organisation’s relationship with the natural world. In Australia, this encompasses greenhouse gas emissions (Scope 1, 2 and 3), climate-related physical and transition risks, energy and water consumption, waste and circular economy practices, biodiversity impacts, and your trajectory toward net zero by 2050.

Australia’s exposure to climate risk is acute — from bushfire and flood to reef degradation and agricultural disruption. The environmental pillar isn’t abstract; it maps directly onto material financial risks that regulators, investors and insurers are already pricing.

Social

The social pillar covers your relationships with people — employees, contractors, supply chain workers, customers and the communities your business operates within. Key areas include workplace health and safety, workforce diversity and pay equity, modern slavery and ethical supply chains, First Nations engagement, customer wellbeing, and community investment.

Australia has some of the most comprehensive social legislation in the world. The Fair Work Act, Work Health and Safety legislation, the Modern Slavery Act, WGEA reporting requirements and the Australian Privacy Principles all create binding obligations that sit squarely within the social pillar.

Governance

Governance is the structural foundation that determines whether your environmental and social commitments are genuine or performative. It encompasses board composition and independence, executive accountability and remuneration structures, risk management frameworks, anti-bribery and corruption policies, whistleblower protections, and the quality and accuracy of your external reporting.

Here’s the thing most businesses underestimate: poor governance is the root cause of most high-profile ESG failures. When companies misrepresent their sustainability credentials, cut corners on safety or enable unethical supply chain practices, it’s almost always a governance failure at the core.

Why ESG Matters for Australian Businesses in 2026

Australia’s ESG regulatory environment has undergone fundamental transformation since 2023. Five developments stand out as particularly significant for business leaders right now.

Mandatory Climate Disclosure Is Law

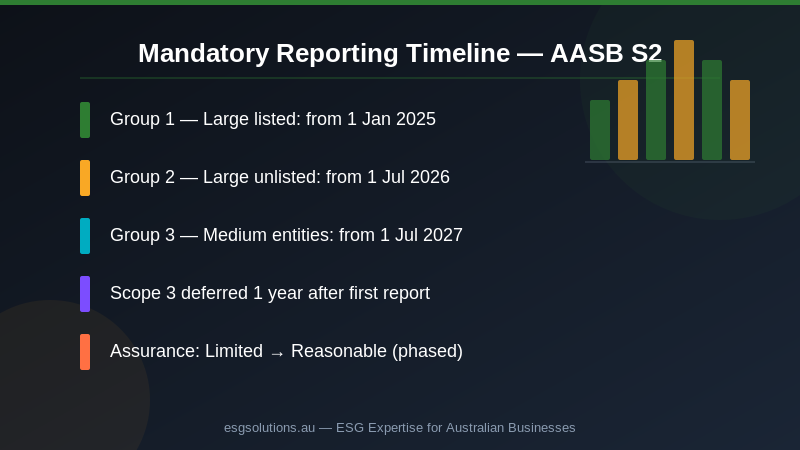

The Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 introduced staged mandatory climate disclosure requirements aligned with AASB S1 and AASB S2 — Australia’s adoption of the international ISSB standards (IFRS S1 and IFRS S2).

The three-group staging is:

- Group 1 (large listed entities, large financial institutions, large superannuation funds): annual reporting periods beginning on or after 1 January 2025

- Group 2 (large unlisted entities meeting size thresholds): annual periods beginning on or after 1 July 2026

- Group 3 (medium entities and others): annual periods beginning on or after 1 July 2027

For Group 1 entities, the full disclosure regime — including Scope 1, 2 and 3 emissions, climate scenario analysis, transition plan disclosures and governance of climate risk — is already in force.

ASIC Is Actively Enforcing Against Greenwashing

ASIC’s greenwashing enforcement activity has accelerated substantially. The regulator has taken action against investment managers, financial products and corporate entities for misleading sustainability claims — securing infringement notices, court enforceable undertakings and civil penalties. ASIC’s Information Sheet 271 (INFO 271) provides detailed guidance on what constitutes a sustainable, responsible or ethical claim — and what evidence you need to substantiate it.

The core test is simple: if your ESG claims can’t be supported by evidence, you’re at legal risk under the Corporations Act and the ASIC Act. Every board and marketing team should have reviewed INFO 271.

APRA Has Embedded Climate Risk in Prudential Supervision

APRA’s Prudential Practice Guide CPG 229 on Climate Change Financial Risks requires regulated entities — banks, insurers and superannuation funds — to have credible frameworks for identifying, assessing and managing climate-related financial risks. This flows directly into how these institutions assess the businesses they finance, insure and invest in. If your ESG credentials are weak, your cost of capital and insurance may reflect it.

Investor Expectations Have Shifted Permanently

Australia’s major institutional investors — including the Future Fund, Australian superannuation funds and international asset managers — have published detailed ESG integration policies. Many now apply screens that exclude businesses with poor ESG ratings or insufficient climate disclosure. The UNPRI (Principles for Responsible Investment) has over 5,000 signatories globally, collectively managing more than USD $120 trillion — and they require signatories to embed ESG considerations across their investment decision-making.

Workforce and Customer Expectations

Younger workers, in particular, increasingly factor employer ESG credentials into their employment decisions. Research consistently shows that purpose-driven organisations attract and retain talent more effectively. Similarly, B2B customers — especially large corporates managing their own Scope 3 emissions — are asking suppliers to demonstrate credible environmental management. ESG has become a procurement filter.

The Environmental Pillar: Australia’s Climate and Sustainability Obligations

Australia sits among the world’s highest per-capita emitters and faces disproportionate physical climate risks. Managing the environmental pillar in the Australian context requires attention to three distinct areas.

Greenhouse Gas Emissions and the Safeguard Mechanism

Australia’s National Greenhouse and Energy Reporting (NGER) Act requires large industrial facilities to report emissions annually. The Safeguard Mechanism applies declining baselines to Australia’s largest emitters — those emitting more than 100,000 tonnes of CO2-equivalent per year — creating a compliance obligation and a market for Australian Carbon Credit Units (ACCUs).

But the Safeguard Mechanism is only the floor. Under AASB S2, disclosing entities must report Scope 1, 2 and — after a short transition period — Scope 3 emissions, conduct climate scenario analysis using 1.5°C and higher-warming scenarios, and disclose a credible transition plan. The emissions reporting requirements extend well beyond those covered by NGER.

Physical and Transition Climate Risks

AASB S2 requires businesses to assess and disclose both physical and transition climate risks:

- Physical risks: acute events (cyclones, floods, bushfires, heatwaves) and chronic changes (sea level rise, shifting agricultural zones, increased average temperatures)

- Transition risks: policy and regulatory changes (carbon pricing, mandatory disclosure), technology changes (rapid renewable energy deployment, electrification), and market shifts (changing customer preferences, stranded assets)

Australian businesses in property, agriculture, resources, construction and coastal tourism face material physical risk exposures that need to be quantified and disclosed.

Net Zero and Science-Based Targets

Australia’s Nationally Determined Contribution (NDC) under the Paris Agreement commits to a 43% reduction in emissions below 2005 levels by 2030, and net zero by 2050. The Climate Change Act 2022 legislates this commitment. For businesses, alignment with Australia’s net zero trajectory requires setting credible, time-bound emissions reduction targets — ideally science-based targets (SBTs) validated by the Science Based Targets initiative (SBTi).

The Social Pillar: People, Community and Ethical Supply Chains

Australia’s social pillar is shaped by a rich body of legislation — but most organisations have social data scattered across HR, procurement and legal rather than consolidated into a coherent ESG view.

Workplace Health and Safety

Under harmonised WHS legislation — which has been adopted in most Australian jurisdictions — employers have a primary duty of care to eliminate or minimise risks to workers as far as reasonably practicable. Leading ESG frameworks track LTIFR (Lost Time Injury Frequency Rate), TRIFR (Total Recordable Injury Frequency Rate), near-miss reporting rates and safety culture survey scores. WHS performance is both a legal requirement and a meaningful ESG indicator.

Workforce Diversity, Equity and Inclusion

WGEA reporting requirements apply to private sector employers with 100 or more employees. Since 2024, WGEA publishes employer-level gender pay gap data publicly — a significant step up in transparency pressure. Beyond WGEA, the Fair Work Act and federal anti-discrimination legislation create a comprehensive framework. ESG social disclosures should address gender representation across seniority levels, pay equity, First Nations employment and supplier diversity, and inclusion metrics (engagement, psychological safety scores).

Modern Slavery and Ethical Supply Chains

The Modern Slavery Act 2018 requires Australian entities with annual consolidated revenue of $100 million or more to publish an annual Modern Slavery Statement covering how they identify, assess and address modern slavery risks in their operations and supply chains. The definition of modern slavery covers forced labour, child labour, human trafficking, debt bondage, servitude and other forms of exploitation.

Even below the $100M threshold, the expectation of modern slavery due diligence is now embedded in large corporate procurement processes. Supplier questionnaires, contractual labour standards clauses and periodic audits are increasingly standard practice.

First Nations Engagement

Australia’s historical context with First Nations peoples creates a specific social responsibility that is increasingly embedded in ESG frameworks. Leading practice includes cultural heritage assessments for land-related activities, supplier diversity programs that include Indigenous-owned businesses, reconciliation action plans (RAPs) developed with the Reconciliation Australia framework, and genuine consultation on projects affecting First Nations communities.

The Governance Pillar: Leadership, Accountability and Ethics

The governance pillar determines whether your ESG strategy is genuine or cosmetic. Sophisticated investors can identify the difference quickly — and regulators can prove it in court.

Board Composition and ESG Oversight

The ASX Corporate Governance Principles and Recommendations (4th edition, 2019) recommend that the majority of a listed company’s board consist of independent directors, that the Chair and CEO roles are separated, that the board undertakes regular skills assessments, and that diversity across gender, culture and experience is valued. Best practice now adds: at least one board member with relevant sustainability expertise, and a dedicated board committee or clearly defined board function overseeing ESG risks and opportunities.

Executive Remuneration and ESG Linkage

A growing proportion of ASX companies now link a component of executive variable remuneration to ESG performance targets. The most common metrics are emissions reduction targets, safety outcomes (LTIFR), and diversity KPIs. This linkage signals to investors that the organisation’s leadership has personal accountability for ESG outcomes — not just aspirational language in the annual report.

Risk Management Frameworks

AASB S2 requires disclosing entities to explain how climate risk is identified, assessed and managed, and how this integrates with overall enterprise risk management. The ISO 31000 risk management standard provides a widely used framework for this integration. ESG risks — including climate risk, regulatory compliance risk, supply chain risk and reputational risk — should sit in the enterprise risk register, with clear ownership, escalation paths and board-level visibility.

Whistleblower Protections and Ethics Culture

Australia’s Treasury Laws Amendment (Enhancing Whistleblower Protections) Act 2019 introduced strong protections for eligible disclosers in the corporate and financial sector. Regulated entities must have a compliant whistleblower policy. Beyond legal compliance, a genuine ethics culture — supported by a code of conduct, anti-bribery and corruption training, and an accessible reporting mechanism — is a hallmark of strong ESG governance.

ESG Reporting Frameworks Used in Australia

Australian businesses now have multiple reporting frameworks in play. Here’s how the key ones relate to each other:

| Framework | What It Covers | Mandatory? |

|---|---|---|

| AASB S1 / AASB S2 | General sustainability disclosures + climate disclosures | Yes — staged by entity size |

| TCFD | Climate-related financial disclosures | Aligned with AASB S2 |

| GRI Standards | Broad ESG disclosure across all sectors | Voluntary — widely used |

| ISSB (IFRS S1/S2) | Global sustainability baseline (adopted via AASB) | Via AASB S1/S2 |

| UN SDGs | 17 Sustainable Development Goals alignment | Voluntary |

| Modern Slavery Act | Supply chain labour risk reporting | Mandatory — ≥$100M revenue |

| WGEA | Gender equality indicators and pay gap reporting | Mandatory — ≥100 employees |

| NGER | Greenhouse gas and energy reporting | Mandatory — large emitters |

For most Australian businesses, a GRI-aligned materiality assessment provides the broadest ESG coverage and the most stakeholder-relevant structure. AASB S2 preparation should run in parallel if you’re approaching mandatory reporting thresholds. The two frameworks are complementary, not competing.

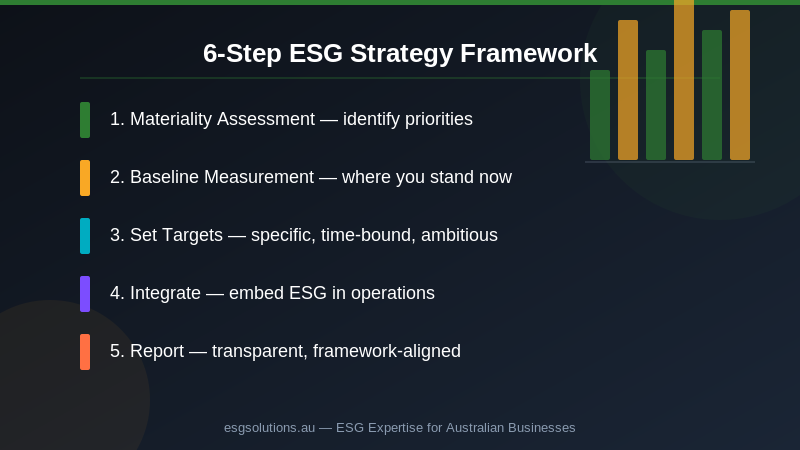

How to Build an ESG Strategy for Your Australian Business

A practical ESG strategy isn’t a standalone document produced once a year — it’s an integrated management system with measurable commitments, clear ownership and credible external reporting. Here’s a six-step framework suited to the Australian context.

Step 1: Conduct a Materiality Assessment

A materiality assessment identifies which ESG issues are most significant for your business and your stakeholders. Under the GRI framework, this involves a double materiality lens — assessing both the impact your business has on the environment and society, and the financial impact that ESG risks and opportunities have on your business. AASB S2 focuses primarily on financial materiality from a climate perspective.

Stakeholder engagement — interviews, surveys, and consultation with employees, investors, customers, suppliers and community representatives — is an essential input. The output should be a ranked matrix of material ESG topics that informs your strategy and reporting priorities.

Step 2: Establish Your Baseline

Before you can set targets, you need to know where you stand. Your baseline should cover:

- A greenhouse gas inventory (at minimum Scope 1 and 2; Scope 3 for high-priority categories)

- An assessment of your governance framework against ASX CGC Principles and AASB S2 governance requirements

- A social data audit: workforce diversity ratios, pay equity analysis, WHS statistics, Modern Slavery exposure map

- An inventory of your current ESG policies, certifications and commitments

Step 3: Set Meaningful Targets

Targets should be specific, measurable, time-bound and ambitious. For emissions, science-based targets are the gold standard — validated pathways to net zero consistent with limiting global warming to 1.5°C above pre-industrial levels. For social indicators, targets might include DEI representation milestones, LTIFR reduction targets, Modern Slavery supplier audit coverage, and gender pay equity ratios. Governance targets could include board skills matrix completion, whistleblower policy implementation, and ESG risk register integration timelines.

Step 4: Integrate ESG Into Operations

The most common ESG failure mode is the “sustainability silo” — where environmental and social management is handled by a dedicated team with limited influence over operational and capital allocation decisions. Effective ESG integration embeds sustainability criteria into strategic planning, procurement decisions, capital expenditure assessments, performance management and new product or market entry assessments.

Step 5: Report and Communicate

Transparency is the foundation of ESG credibility. Annual ESG or sustainability reports aligned to GRI and (where applicable) AASB S1/S2 provide a structured way to communicate your strategy, progress and challenges to all stakeholders. Be honest about gaps and underperformance — stakeholders respond more positively to genuine accountability than to airbrushed progress narratives.

Step 6: Seek Assurance

External assurance of ESG data — particularly climate disclosures under AASB S2 — provides credibility and helps identify data quality issues before they become regulatory or reputational problems. AASB S2 requires limited assurance initially, with reasonable assurance phased in over time. Start building your data collection, verification and governance processes now, well before your mandatory reporting date.

ESG for Australian SMEs: Starting Simple, Building Progressively

A common misconception is that ESG is only for large listed companies. The reality is that ESG expectations are flowing through supply chains, procurement processes and financing arrangements to businesses of all sizes. Here’s what that means in practice for Australian SMEs.

Your large corporate clients are applying Scope 3 accounting — meaning they need emissions data from their suppliers. Institutional investors are asking portfolio companies to report on supply chain ESG risks. Government procurement policies in many jurisdictions now include sustainability criteria. And talent acquisition data consistently shows that purpose-driven organisations attract stronger candidates, particularly from younger cohorts.

A pragmatic ESG starting point for an Australian SME includes:

- A documented Scope 1 and 2 emissions baseline — even an approximate calculation is a starting point

- A Modern Slavery Statement if you meet the $100M threshold, or a documented supply chain risk assessment if you don’t

- An up-to-date WHS management system with recorded performance metrics

- Basic governance documentation: code of conduct, conflict of interest policy, whistleblower policy, risk register

- A DEI statement with at least some baseline workforce diversity data

This foundation can be built progressively — adding depth, rigour and breadth as regulatory expectations mature and as you develop internal capacity.

Common ESG Mistakes Australian Businesses Make

Watching what doesn’t work is as instructive as knowing what does. Here are the most common pitfalls in Australian ESG practice.

Greenwashing

Making sustainability claims that your evidence can’t support. ASIC is actively pursuing greenwashing cases. The legal risk under the Corporations Act and ASIC Act is real — as is the reputational risk when claims are scrutinised publicly. If you can’t substantiate a claim with specific, up-to-date data, don’t make it.

Treating ESG as a Compliance Exercise

Filing a WGEA report, ticking the Modern Slavery Statement box and publishing a sustainability page is not an ESG strategy. Sophisticated stakeholders — investors, large customers, regulators — can identify quickly when ESG is performative rather than integrated. The businesses gaining competitive advantage from ESG are those where sustainability is genuinely embedded in strategy and operations.

Neglecting Scope 3 Emissions

Many organisations complete a Scope 1 and 2 inventory and consider the carbon picture substantially complete. For most Australian businesses, Scope 3 is where the largest emissions volumes sit — in purchased goods, logistics, customer use and end-of-life disposal. Ignoring Scope 3 also means ignoring a significant source of transition risk (as regulations tighten) and opportunity (from supply chain decarbonisation).

Weak Governance Foundations

Environmental and social commitments without strong governance to back them up are empty promises. Investors and regulators increasingly look at governance quality as the leading indicator of ESG credibility — because good governance is what ensures the other commitments are genuinely pursued and accurately reported.

The Future of ESG in Australia: What to Watch

The Australian ESG regulatory and market landscape will continue to evolve rapidly. Several near-term developments deserve particular attention.

Scope 3 mandatory disclosure is expected to become a firm requirement as AASB S2 implementation matures and the transitional relief provisions expire. Businesses that have started their Scope 3 measurement journey now will be significantly better placed.

Nature-related financial disclosures — following the TNFD framework — are gaining momentum globally and are expected to be incorporated into Australian reporting expectations. Businesses with material exposure to land, water, biodiversity or agricultural supply chains should begin their nature-related risk assessments now.

Social value accounting — quantifying the economic and social value generated by business activities for communities — is increasingly applied in infrastructure, government procurement and community-facing industries.

AI and digital ethics governance is emerging as a new ESG frontier. As AI systems play a larger role in recruitment, customer decisions and operational management, questions of algorithmic bias, data privacy, transparency and digital rights are becoming material ESG governance issues.

Modern Slavery Act review — the Australian Government has announced a review of the Modern Slavery Act, with recommendations expected to include lowering the revenue threshold and strengthening due diligence requirements. Businesses below the current $100M threshold should prepare now.

Frequently Asked Questions About ESG in Australia

Is ESG reporting mandatory in Australia?

Yes — mandatory climate disclosure requirements under AASB S1 and AASB S2 are now in force for Group 1 entities (large listed companies and financial institutions from 1 January 2025). Group 2 and Group 3 entities face mandatory requirements from 2026 and 2027 respectively. Separate mandatory obligations apply under the Modern Slavery Act (revenue ≥$100M), WGEA (≥100 employees) and NGER (large emitters).

What is the difference between ESG and sustainability?

ESG and sustainability are closely related but not identical. Sustainability is a broader concept encompassing long-term business viability and responsible stewardship of environmental, social and economic resources. ESG is a structured framework for measuring, managing and reporting on specific environmental, social and governance indicators — primarily for the benefit of investors and other external stakeholders. All ESG activity sits within a broader sustainability agenda, but not all sustainability activities are captured by ESG metrics.

What is AASB S2 and does it apply to my business?

AASB S2 is the Australian Accounting Standards Board’s standard on Climate-related Disclosures, aligned with the ISSB’s IFRS S2. It applies to entities that are required to lodge financial reports under Chapter 2M of the Corporations Act and that meet size thresholds as described in the staged implementation. AASB S2 requires disclosures on climate-related governance, strategy, risk management, and metrics and targets — including Scope 1, 2 and 3 emissions.

How much does it cost to develop an ESG strategy?

The cost of ESG strategy development varies significantly with organisational size and complexity. An SME developing a foundational ESG framework might invest $15,000–$50,000 with external advisory support. A mid-market company preparing for mandatory AASB S2 disclosure might invest $100,000–$300,000 in gap analysis, materiality assessment, data systems and reporting. Large listed entities are typically investing seven figures annually in ESG management and reporting. The cost of not having a credible ESG strategy — in terms of investor relations, customer relationships and regulatory risk — increasingly exceeds the cost of building one.

Start Your ESG Journey with ESG Solutions

ESG in Australia is not a destination — it’s an ongoing journey that requires strategy, data, governance and genuine commitment. The organisations that will come out ahead are those building credible ESG foundations now, not waiting until mandatory deadlines force the issue.

At ESG Solutions, we work with Australian businesses across every stage of the ESG journey — from initial materiality assessments and baseline measurement through to integrated strategy development, reporting framework implementation and external assurance readiness.

Whether you’re a large listed entity navigating AASB S2 for the first time or an SME looking to build a credible sustainability foundation, we have the expertise to help you do it right.

Book a Free ESG Strategy Session with our team today — no obligation, just a clear picture of where you stand and what to prioritise next.