The Australian Sustainability Reporting Standards (ASRS) represent a transformative shift in corporate disclosure requirements. From 2025, large Australian entities must report on climate-related financial information, marking the most significant change to corporate reporting in decades.

What is ASRS Sustainability Reporting?

The Australian Sustainability Reporting Standards (ASRS) are mandatory climate disclosure standards developed by the Australian Accounting Standards Board (AASB). These standards align with international frameworks including the IFRS Sustainability Disclosure Standards and the Task Force on Climate-related Financial Disclosures (TCFD).

ASRS reporting requirements establish a consistent framework for organisations to disclose climate-related risks, opportunities, and financial impacts. This enables investors, regulators, and stakeholders to make informed decisions about an entity’s climate resilience and transition strategy.

ASRS Reporting Timeline and Phased Implementation

The ASRS implementation follows a phased approach based on entity size and reporting obligations:

Group 1: Large Entities (2025-2026)

Entities meeting two of three criteria begin mandatory reporting for financial years starting from 1 January 2025:

- Consolidated revenue of $500 million or more

- Consolidated gross assets of $1 billion or more

- 500 or more employees

This includes Australia’s largest listed companies, financial institutions, and significant private entities. These organisations must prepare for compliance ahead of their first reporting period.

Group 2: Medium Entities (2026-2027)

Entities meeting two of three thresholds commence reporting for financial years starting from 1 July 2026:

- Consolidated revenue of $200 million or more

- Consolidated gross assets of $1 billion or more

- 250 or more employees

This captures mid-tier ASX-listed companies, large private businesses, and significant subsidiaries of multinational corporations.

Group 3: Smaller Entities (2027-2028)

Entities meeting two of three criteria from 1 July 2027:

- Consolidated revenue of $50 million or more

- Consolidated gross assets of $25 million or more

- 100 or more employees

Even smaller entities should consider voluntary adoption to demonstrate leadership and prepare for future regulatory expansion.

Core ASRS Disclosure Requirements

ASRS sustainability reporting encompasses four fundamental pillars aligned with TCFD recommendations:

1. Governance Disclosures

Organisations must disclose how climate-related risks and opportunities are overseen by the board and management. This includes:

- Board composition and climate competence

- Management’s role in assessing and managing climate risks

- Processes for informing the board about climate matters

- How climate considerations inform strategic decisions

Effective governance demonstrates that climate risk is embedded in organisational decision-making at the highest level.

2. Strategy Disclosures

Climate-related risks and opportunities must be disclosed alongside their impact on the organisation’s strategy and financial planning. Required elements include:

- Current and anticipated climate-related risks and opportunities

- Impact on business model and value chain

- Effects on strategy and financial planning

- Climate scenario analysis and resilience assessment

Strategy disclosures connect climate risk to business strategy, demonstrating how organisations are positioning for a low-carbon transition.

3. Risk Management Disclosures

Entities must describe processes for identifying, assessing, and managing climate-related risks. This encompasses:

- Physical risk identification and assessment

- Transition risk evaluation across multiple scenarios

- Integration with enterprise risk management frameworks

- Litigation and liability risk considerations

Comprehensive risk management demonstrates mature climate governance and builds stakeholder confidence.

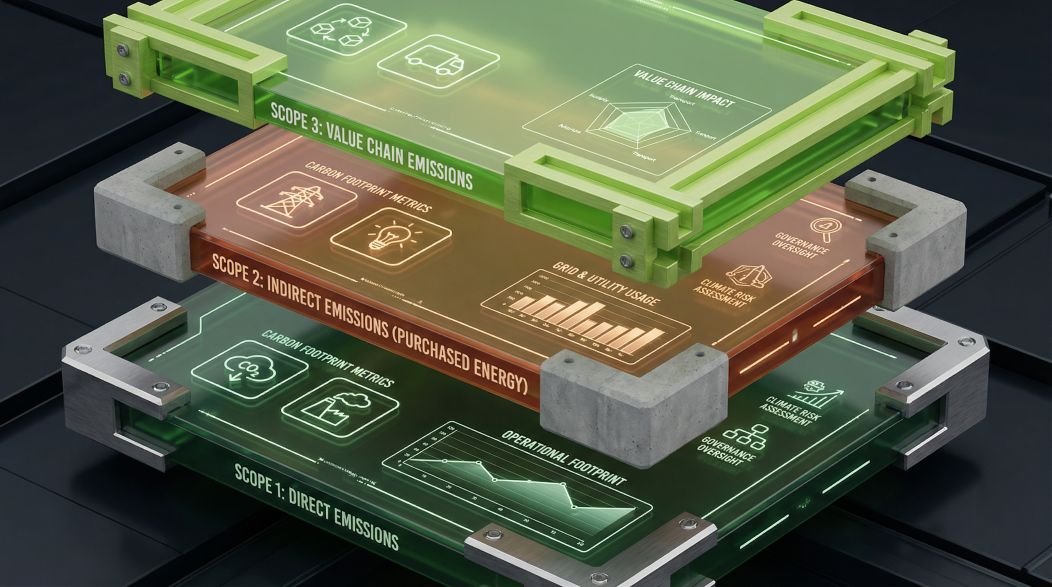

4. Metrics and Targets Disclosures

Quantitative disclosures provide the empirical foundation for climate reporting. Requirements include:

- Scope 1, Scope 2, and material Scope 3 greenhouse gas emissions

- Climate-related targets and progress against them

- Internal carbon prices and their application

- Climate-related financial metrics and remuneration links

Metrics and targets enable stakeholders to assess performance and track progress toward climate commitments.

ASRS vs GRI vs TCFD Framework Comparison

Understanding the relationship between ASRS and other sustainability frameworks is essential for comprehensive reporting:

| Framework | Focus | Scope | Status in Australia |

|---|---|---|---|

| ASRS | Climate-related financial disclosure | Mandatory for qualifying entities | Phased implementation from 2025 |

| GRI | Broad sustainability reporting | Voluntary best practice | Widely adopted by ASX entities |

| TCFD | Climate risk framework | Voluntary, now embedded in ASRS | Foundation for ASRS structure |

Many organisations already reporting under GRI or TCFD will find ASRS builds upon existing frameworks rather than replacing them. The key difference is ASRS mandates consistent, comparable climate disclosure across Australian reporting entities.

Preparing for ASRS Compliance

Organisations approaching ASRS reporting should systematically address key readiness areas:

Gap Assessment and Baseline Analysis

Conduct a comprehensive gap assessment against ASRS requirements. This identifies areas where existing reporting processes, data collection, and governance structures require enhancement. A baseline analysis establishes current capabilities and prioritises improvement actions.

Data Collection and Systems

Climate disclosure requires robust data systems for emissions calculation, scenario modelling, and performance tracking. Organisations should:

- Implement emissions measurement across Scope 1, 2, and 3

- Develop value chain data collection processes

- Establish internal controls for sustainability data

- Consider specialised ESG reporting software

Data quality is paramount for credible disclosure and regulatory compliance.

Climate Scenario Analysis

ASRS requires climate scenario analysis to assess organisational resilience. This involves modelling business exposure under different climate pathways, typically including:

- A 1.5°C or well-below 2°C scenario aligned with Paris Agreement goals

- A 2-3°C scenario reflecting current policy trajectories

- A higher-warming scenario (3-4°C) for physical risk assessment

Scenario analysis reveals strategic vulnerabilities and informs transition planning.

Double Materiality Assessment

ASRS incorporates the concept of double materiality—the principle that organisations should report on matters that affect enterprise value (financial materiality) AND matters where the organisation impacts environment or society (impact materiality).

Conducting a double materiality assessment ensures comprehensive identification of reportable matters. This process involves:

- Stakeholder engagement and concern mapping

- Environmental and social impact evaluation

- Financial risk and opportunity identification

- Prioritisation of material topics for disclosure

Double materiality aligns ASRS with European sustainability reporting standards and positions organisations for evolving global requirements.

Common ASRS Reporting Challenges

Organisations frequently encounter these challenges when implementing ASRS:

- Scope 3 emissions measurement: Value chain emissions require supplier engagement and estimation methodologies that many organisations lack

- Climate scenario modelling: Quantitative scenario analysis demands specialised expertise and assumptions that affect disclosure comparability

- Board climate competence: Governance disclosures require demonstrable board understanding of climate risk

- Assurance readiness: Climate disclosures will require external assurance, necessitating audit-grade data and documentation

- Transition planning: Disclosing credible decarbonisation pathways requires strategic clarity and measurable targets

Early preparation and expert guidance significantly reduce compliance risk and disclosure quality issues.

Industry-Specific ASRS Considerations

Climate risk and disclosure requirements vary significantly by sector:

Financial Services

APRA-regulated entities have additional prudential requirements for climate risk management. Banks, insurers, and superannuation funds must disclose financed emissions and climate-related financial risks in loan portfolios and investment holdings. See our guidance on ESG reporting for financial services.

Mining and Resources

Mining companies face heightened transition risk scrutiny given emissions intensity and stranded asset exposure. Physical risk from extreme weather events, water stress, and changing operational conditions requires detailed disclosure. Learn more about ESG reporting for mining companies.

Energy and Utilities

Energy sector entities are central to the net-zero transition. Disclosure requirements include asset-level transition pathways, renewable energy investments, and just transition considerations for affected workforces and communities.

How ESG Solutions Can Help

ESG Solutions provides comprehensive ASRS compliance support tailored to Australian organisations:

- Gap assessment and readiness reviews: Evaluate current capabilities against ASRS requirements

- Climate risk assessment: Identify physical and transition risks across your operations and value chain

- Materiality assessment: Conduct double materiality analysis to prioritise disclosure topics

- Emissions measurement: Calculate Scope 1, 2, and 3 emissions using recognised methodologies

- Scenario analysis: Model business resilience under multiple climate pathways

- Disclosure preparation: Develop climate statements aligned with ASRS standards

- Assurance readiness: Prepare documentation for external assurance engagements

Our team combines technical climate expertise with deep understanding of Australian regulatory context. We help organisations move from compliance obligation to strategic advantage through credible, decision-useful climate disclosure.

Explore our full range of ESG services or contact us to discuss your ASRS reporting requirements.

Key Takeaways

- ASRS introduces mandatory climate disclosure for Australian entities from 2025, with phased implementation based on entity size

- Core disclosure pillars align with TCFD: governance, strategy, risk management, and metrics/targets

- Double materiality requires reporting on both financial impacts and environmental/social effects

- Early preparation addresses common challenges including Scope 3 measurement, scenario analysis, and assurance readiness

- Industry-specific considerations affect disclosure priorities and material risk identification